Dear friends,

Welcome to December. Welcome to Winter. It’s my favorite time of the year, despite the post-Covid haze that has enveloped me all week. Augustana is increasingly festive, ringing with the sounds of holiday concerts and celebrations, as well as the definite “click” of another semester coming to its close. My students, with their hummingbird-like metabolisms, are loathe to surrender their shorts and sandals even now.

We annually share the same simple reminder. Winter has always been a dark and drear span. The weather turns against us, and we retreat inward for protection. Gardens lay frozen. Workdays are framed by darkness: dark when we arise, dark when we return home.

The midwinter holidays ahead – not just Christmas but a dozen other celebrations rooted in other cultures and other traditions – are, at base, expressions of gratitude. They occur in the darkest, coldest, most threatening time of year. They occur at the moment when we most need others, and they most need us. No one thrives when they’re alone, and each day brings 14 to 18 hours of darkness. And so we’ve chosen, from time immemorial, to open our hearts, our homes, our arms, and our pantries to friends and strangers alike.

Don’t talk yourself out of that impulse. Don’t worry about whether your gift is glittery (if people actually care about that, you’re sharing gifts with the wrong people) or your meal is perfect (Martha Stewart’s were, and she ended up in the Big House). People most appreciate gifts that make them think of you; give a part of yourself. Follow the Grinch. Take advice from Scrooged. Tell someone they make you smile, hug them if you dare, smile and go.

In this issue of The Observer

Nearly a week after the fact, I continue muddling through Covid’s after-effects. This variant, unlike its predecessors, has left me surprisingly tired and unfocused. I’ll ask your indulgence as I write only a short letter.

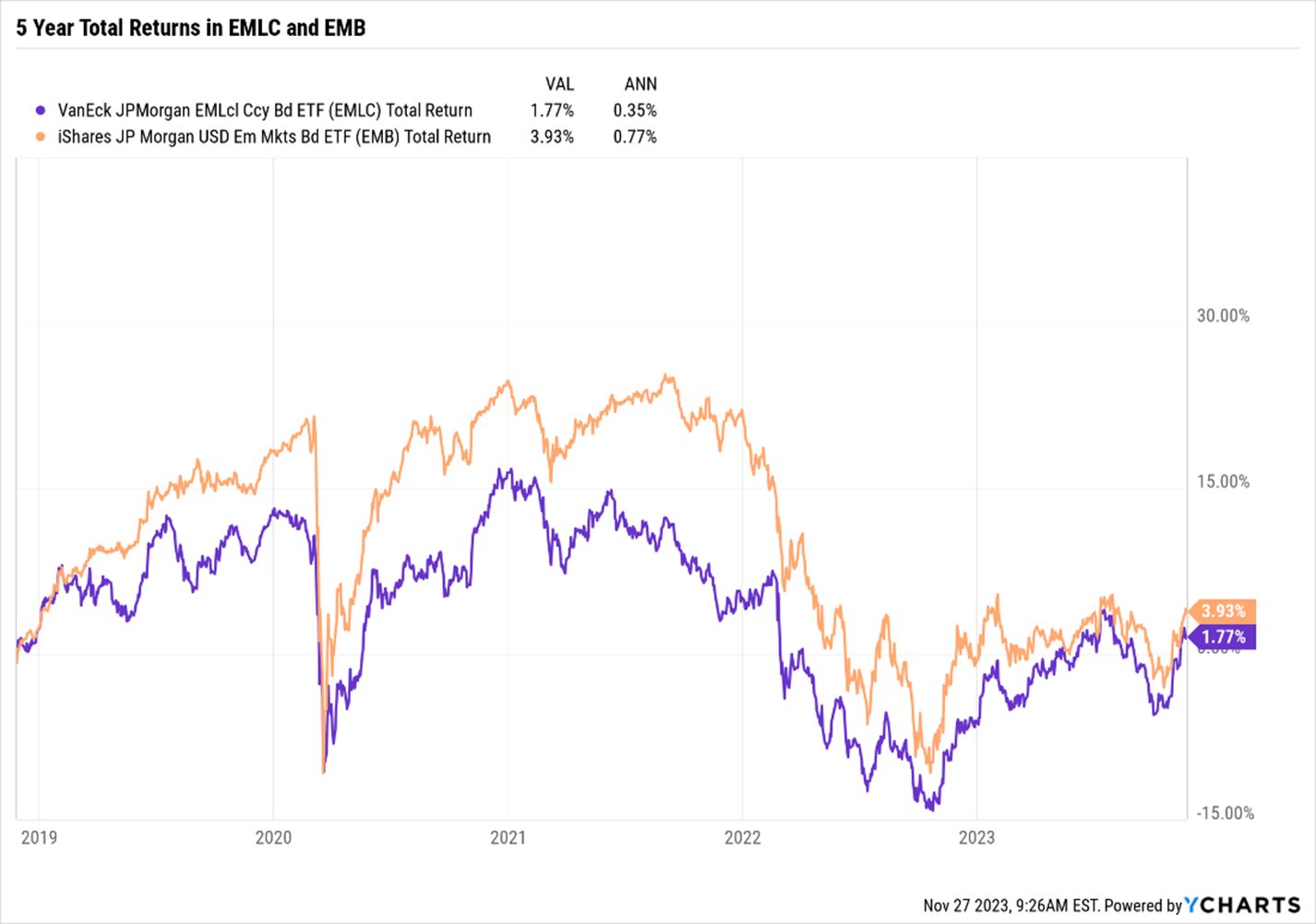

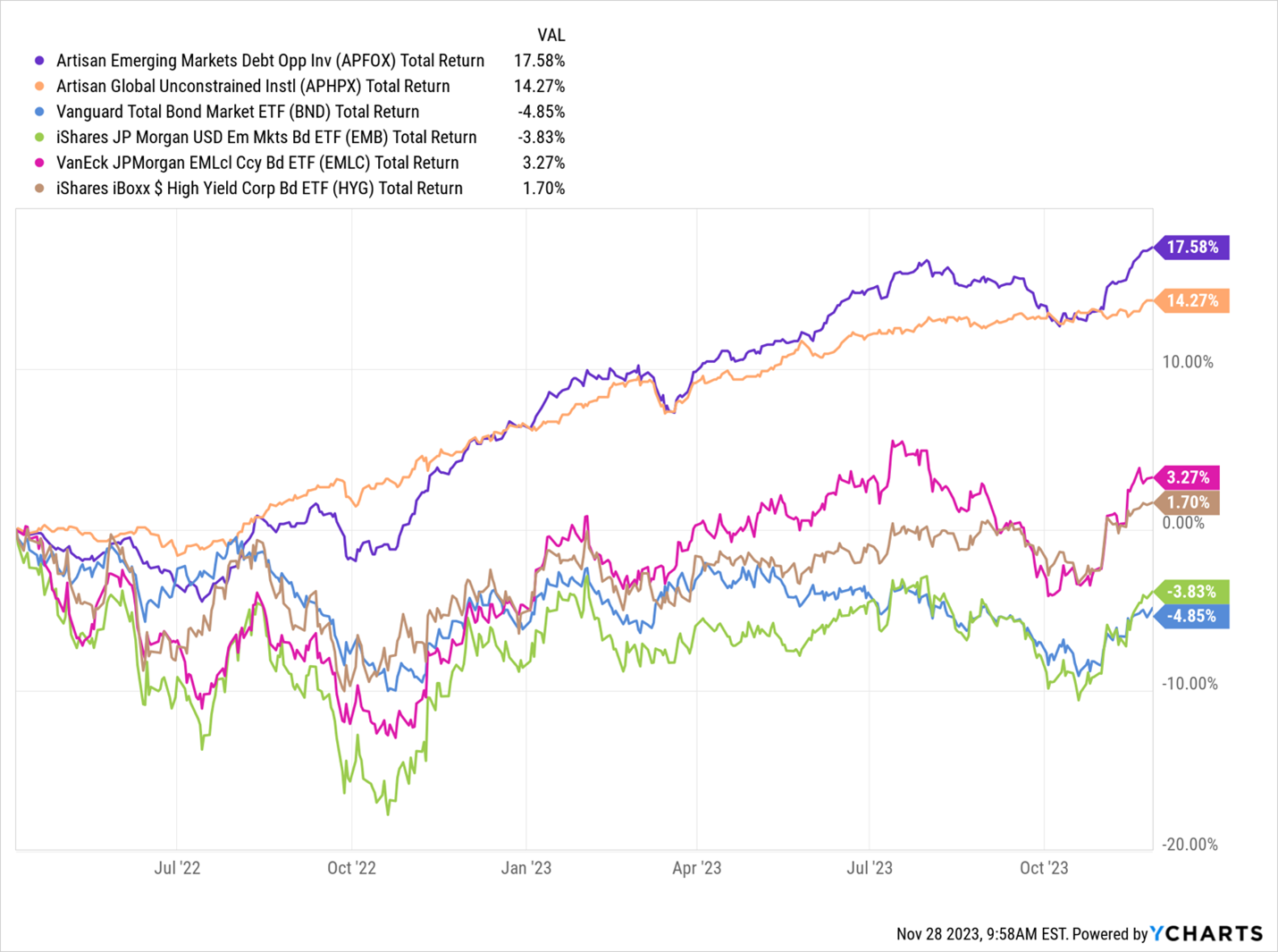

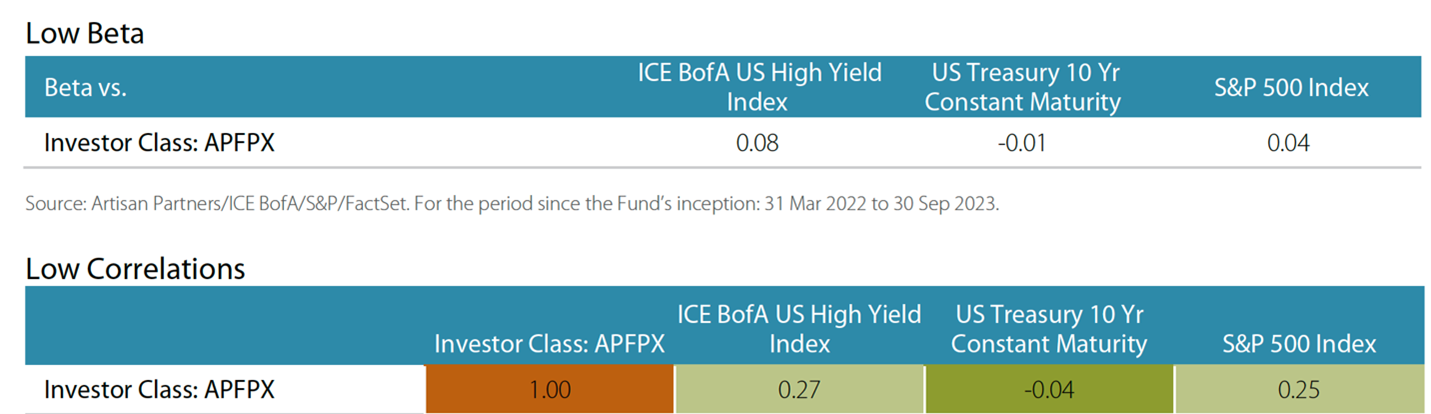

My colleague Devesh Shah had a long and informative interview with one of the industry’s most consistently successful emerging market debt (EMD) investors, Artisan’s Michael Cirami. As a complement to Devesh’s work, I’ve shared a broader piece entitled “Artisan and the Emerging Market Debt Universe.” Read together, they might give you a sense both of the strategy and of its potential role, if any, in your portfolio.

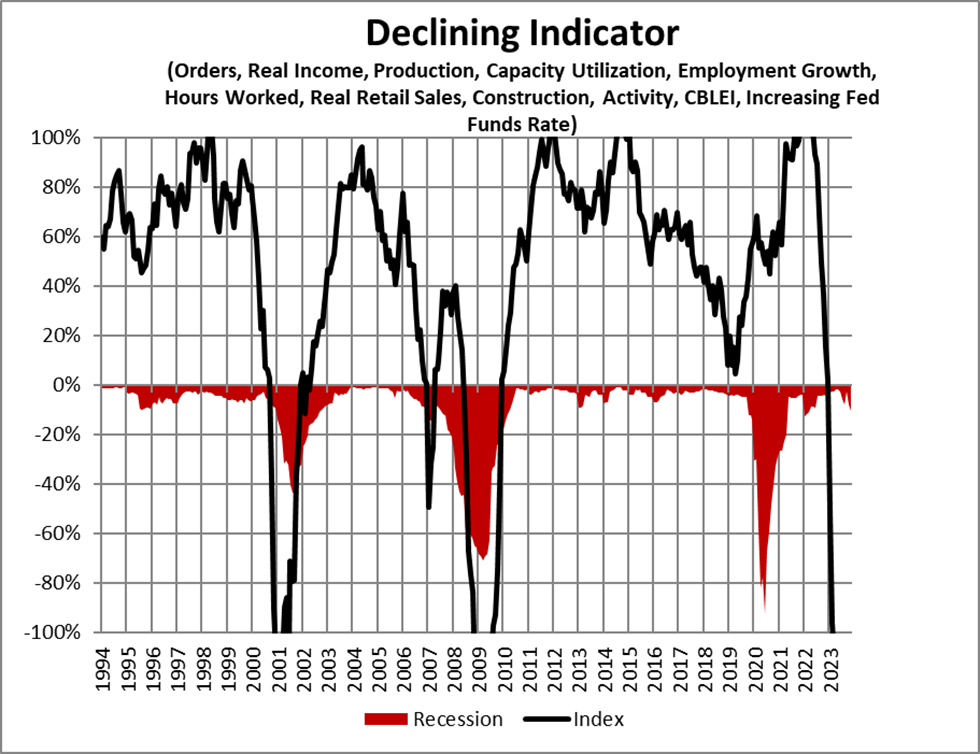

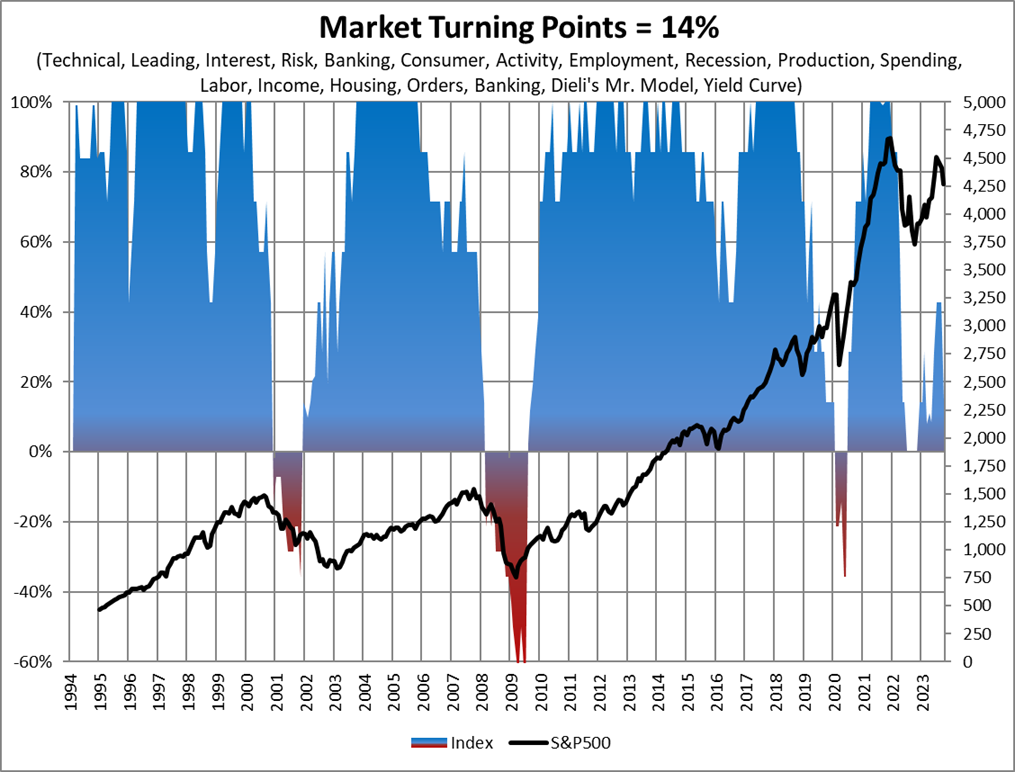

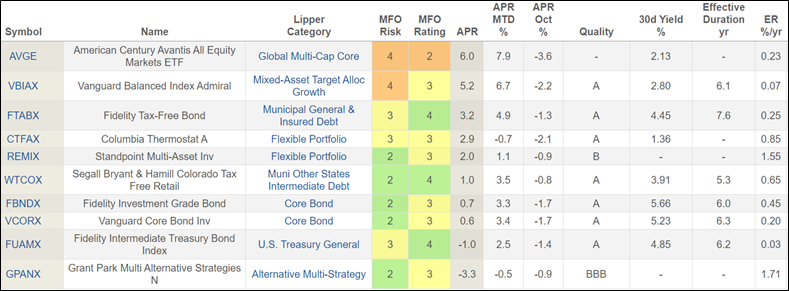

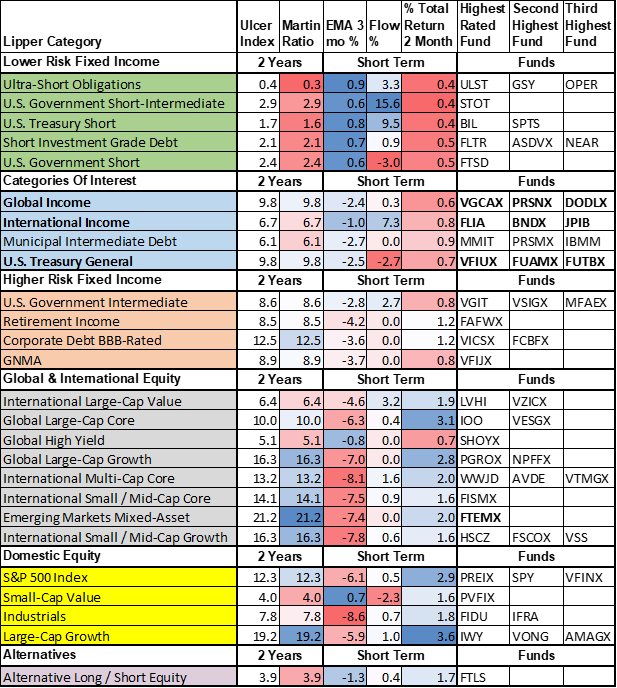

Lynn Bolin went “Searching for Inflection Points.” Lynn understands that the results of what we’ve called The Great Distortion are unsustainable; it is vanishingly unlikely that a handful of high-growth US tech stocks will dominate the global market in the decade ahead. Lynn’s analysis has led him to attractive opportunities in global bond and long-duration funds, and possibly to international equities. His question this month is, “Is it yet time to pull the trigger?”

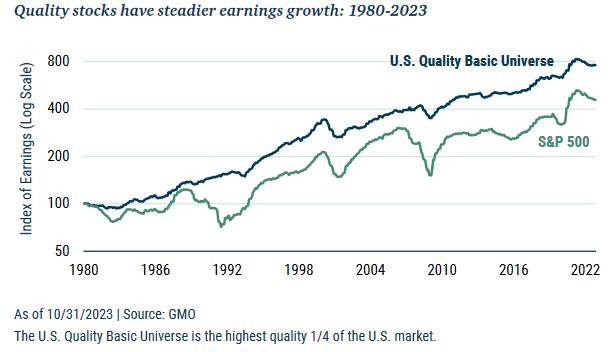

November also saw the debut of two potentially outstanding funds. GMO US Quality ETF, an actively managed ETF, is GMO’s first retail offering. It embodies the Quality Equity strategy that its Focused Equity team has used in the five-star GMO Quality Fund, whose investment minimum runs between $1,000,000 and $500,000,000 depending on the share class.

T. Rowe Price Capital Appreciation and Income Fund completes a suite of Capital Appreciation funds from T. Rowe. The driver is the long-closed, five-star Capital Appreciation Fund, whose performance record is unparalleled. Rather than reopen a $54 billion fund, manager David Giroux has been working at the margins. T. Rowe Price Capital Appreciation Equity ETF, launched last summer, follows – but does not clone – the equity discipline in the original fund. The new Capital Appreciation and Income fund adds two further twists: while it uses the Cap App stock discipline, it has a far heavier weight in fixed income, and it introduces Mr. Giroux’s first co-manager, who is responsible for bringing quant insights into the asset allocation.

Charles Boccadoro, the maestro of MFO Premium, is introducing this month both enhanced chart tools and fund flow analytics.

And, as ever, The Shadow tracks down the industry’s highs and lows in Briefly Noted.

Charles Thomas Munger (1/1/1924 – 11/28/2023)

Charlie Munger passed away in November, a month short of his 100th birthday. I never met Mr. Munger and have no original insights to add to the ocean of encomia that he fully deserves.

Charlie Munger passed away in November, a month short of his 100th birthday. I never met Mr. Munger and have no original insights to add to the ocean of encomia that he fully deserves.

For a rich guy, he seemed strikingly sensible. I think out of all of the advice he offered, two pieces most stand out.

-

Don’t get full of yourself. My feelings toward people with half-billion-dollar yachts and $50 million homes alternates between pity and loathing. A centa-billionaire needs a bed no bigger than a pauper’s, and their insistence otherwise speaks to a profound poverty of soul and mind. Mr. Munger’s works are full of cautions about such hubris: “The world is not driven by greed. It’s driven by envy… I have conquered envy in my own life. I don’t envy anybody. I don’t give a damn what someone else has. But other people are driven crazy by it.”

He explained the magic behind the century’s most successful investing tandem this way: “It’s remarkable how much long-term advantage people like us have gotten by trying to be consistently not stupid, instead of trying to be very intelligent.”

Jason Zweig reported on Mr. Munger’s preferred epitaph: “I tried to be useful.” No, Mr. Z. notes, “I was useful,” which is for others to judge, but the humble “I tried” (“Charlie Munger’s Life Was About Way More Than Money,” WSJ.com, 11/29/2023).

-

Keep learning, keep reading widely. “In my whole life, I have known no wise people (over a broad subject matter area) who didn’t read all the time — none, zero.” Even in his 90s, Mr. Munger read widely, sometimes at the rate of a book every two days. “Spend each day trying to be a little wiser than you were when you woke up. Day by day, and at the end of the day – if you live long enough – like most people, you will get out of life what you deserve.”

His advice was the antithesis of the drone’s impulse to read everything that all of your peers and competitors are reading. If you read nothing but what they read, you’ll think nothing but what they think. Read what they abjure! Read history. Read poetry. Read speculative fiction. Read the words of people smarter than you, and grow from each encounter. Don’t worry about why you’re learning or how it will make you rich next year; learn passionately, and your life will be infinitely richer for it.

December 2023 sees the release of an abridged Poor Charlie’s Almanack, originally published in 2005. Mr. Zweig notes, “Existing editions have sold about 175,000 copies in English and 1.2 million copies in Chinese. “It’s very rare for people to have sound judgment and to be untouched by the magnitude of emotions that surround them. You can only do that after years of self-cultivation,” said Li Lu, who runs Himalaya Capital, a global investment firm in Seattle with large holdings in Chinese stocks. “People in China really do regard Charlie as an example of modern Confucianism.”

Morningstar’s warning: You’re not that smart.

“New research from Morningstar reveals a concerning trend: over the past five years, investors in thematic funds lost more than two-thirds of total returns because of poorly timed buys and sells.”

Morningstar’s report, The Big Shortfall, builds off of their long-running Mind the Gap studies to show that investors’ buying and selling habits destroyed considerable value. They find:

- Investors in narrowly focused funds routinely screw themselves with mistimed purchases and sales.

- Investors in narrowly focused ETFs screw themselves more than those in comparable funds because it’s so much easier – and more manly! – to trade ETF shares frequently throughout the day, relentlessly multiplying the cost of overconfidence.

- Investors in Hot! Hot! Hot! funds fared worst of all.

I’ll close with Mr. Munger’s contrary advice: “It’s so simple. You spend less than you earn. Invest shrewdly, and avoid toxic people and toxic activities, and try and keep learning all your life. And do a lot of deferred gratification because you prefer life that way. And if you do all those things, you are almost certain to succeed. And if you don’t, you’re gonna need a lot of luck.”

Thanks, more than ever …

A bunch of kind folks shared both kind words and some end-of-year financial support this month. I’m honored to thank the folks who have, in some cases, supported MFO for more than a decade and returned this month: Leah from Massachusetts (we’ll try!), Michael of Vegas, Richard from Georgia, Santa from the North Pole (ho-ho-ho, Anonymous Sir!), Binod from Houston, Robert of Kirkwood, Mark from Michigan, John from Pensacola, and Kevin from Brooklyn.

To The Faithful Few, whose monthly contributions keep spirits up and the lights on: Wilson, S & F Investment Advisors, Gregory, William, William, Stephen, Brian, David, and Doug. If you’d like to do your part to keep MFO up and running, please click on the “Support Us” link above or join the MFO Premium folks who, for just $120/year, get access to maestro Charles and some of the most advanced search tools available (or, at least, “available for less than the $16,000 that some others charge”).

Wishing you good health and a joyful season,

The fund will be managed by David Giroux, whose other charges include the long-closed T. Rowe Price Capital Appreciation Fund (PRWCX) which he has managed since 2006, and T. Rowe Price Capital Appreciation ETF (TCAF), launched in June 2023. In both cases, he is listed as the sole manager of the fund. The new fund is co-managed by Farris Shuggi, a quantitative analyst who joined Price in 2008. Price refers to these, collectively, as “the Capital Appreciation suite” of funds. Mr. Giroux positions the new fund as most attractive to “clients … who prioritize current income and enhanced capital preservation.”

The fund will be managed by David Giroux, whose other charges include the long-closed T. Rowe Price Capital Appreciation Fund (PRWCX) which he has managed since 2006, and T. Rowe Price Capital Appreciation ETF (TCAF), launched in June 2023. In both cases, he is listed as the sole manager of the fund. The new fund is co-managed by Farris Shuggi, a quantitative analyst who joined Price in 2008. Price refers to these, collectively, as “the Capital Appreciation suite” of funds. Mr. Giroux positions the new fund as most attractive to “clients … who prioritize current income and enhanced capital preservation.”